ECB Rate Decision: Inflation Hits 3.0% in 2026

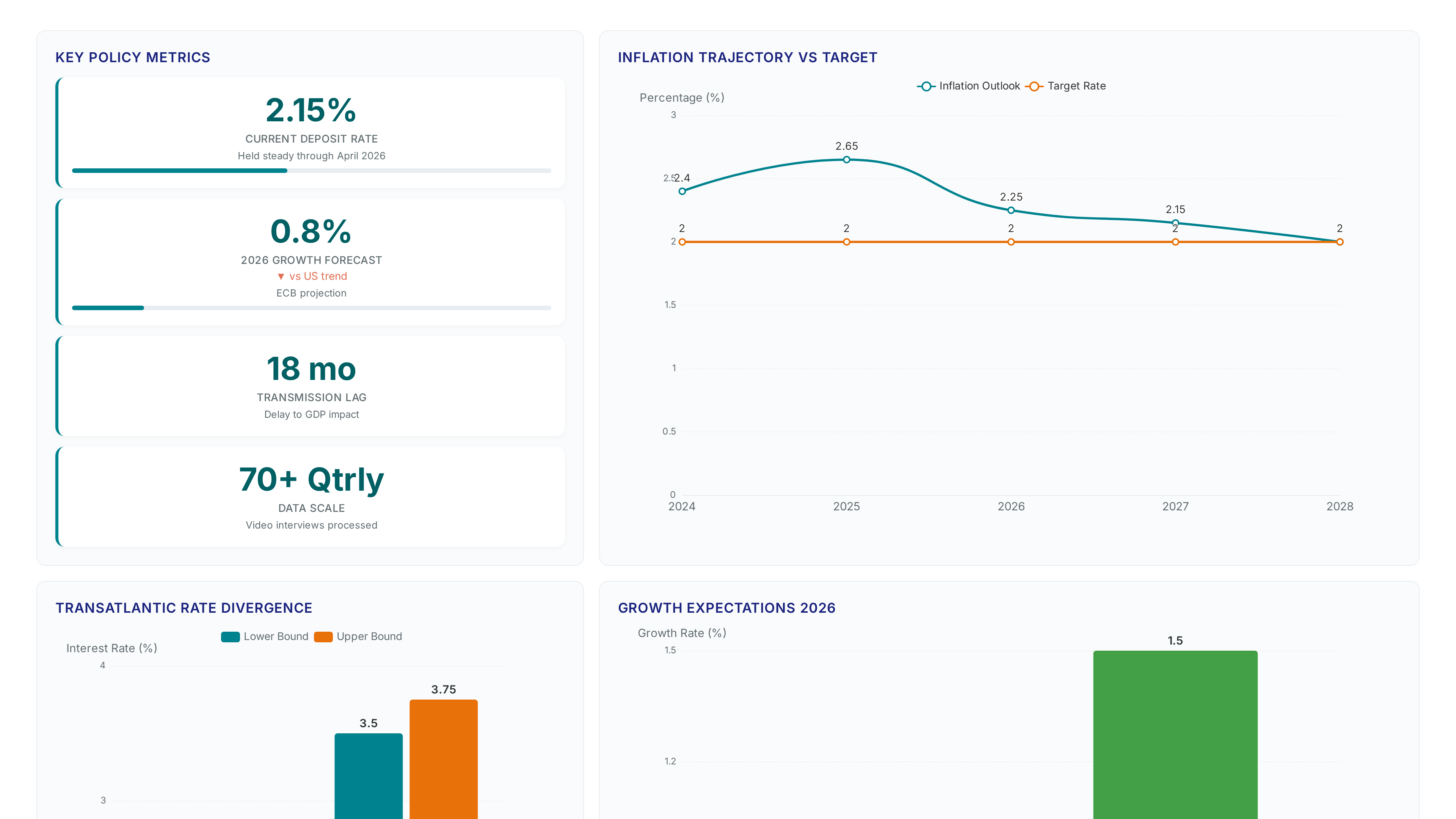

The ECB lifted rates 25 basis points to 2.25%, confirming a decisive shift away from accommodation. energy-driven inflation from the Middle East conflict now dictates monetary policy, forcing the European Central Bank to prioritize price stability over fragile growth. While GDP expansion crawls from 0.8% in 2026 to 1.5% by 2028 per Eurosystem staff projections, the central bank's revised inflation trajectory averaging 3.0% this year demands immediate corrective action. Investors must recognize that the era of cheap capital has paused, with wage dynamics remaining the critical variable preventing a destructive price spiral.

Readers will analyze the mechanics behind the inflation forecast revisions that pushed 2027 expectations to 2.3%, explicitly linking these figures to lingering energy costs. 2% influences the ECB's willingness to hike again in September. Finally, the discussion translates these ECB signals into actionable strategies for navigating sovereign spreads and rate-sensitive assets in a plateauing rate environment through 2027.

The Current ECB Rate Decision and Inflation Forecast Revisions

ECB June 2026 Rate Hike and New Facility Rates

On June 11, 2026, the European Central Bank raised its key interest rate by 25 basis points to 2.25%. The marginal lending facility rate, representing the corridor's upper bound, increased to 2.65%. These levels became proven June 17, 2026, marking the first tightening cycle since 2023. Distinct liquidity pressures now face cross-border treasury operations due to divergence in global monetary policy. The benchmark euro short-term rate stood at 1.93% before the hike, highlighting the sudden shift in funding costs. Operators must model cash flows against a steeper yield curve without assuming rapid reversal. Failure to adjust hedging strategies exposes portfolios to compounded interest expenses as the 25 basis point increase propagates through commercial lending channels. This adjustment period tests liquidity buffers across the eurozone banking sector.

Applying Inflation Forecasts to 2026 and 2027 Economic Outlooks

Revised projections now place the inflation peak at the end of 2026, delaying the return to the 2% target until autumn 2027. This upward revision forces a recalibration of the economic outlook, shifting expectations from a transient spike to a prolonged period of elevated prices. The ECB now anticipates headline HICP inflation averaging 3.0% in 2026, a significant increase from the prior 2.6% estimate. This trajectory implies that real rates will remain restrictive for longer than previously modeled, compressing growth projections to just 0.8% for the current year. Public spending on defense and infrastructure may underpin growth, but these fiscal boosts carry the risk of causing inflation to pick up further over the medium term. Fiscal expansion supports output while monetary tightening attempts to suppress demand, creating a volatile environment for fixed-income portfolios. Consequently, BNP Paribas expects rates to plateau through 2027 following a projected additional hike in September. Operators must treat the higher-for-longer scenario as the baseline, noting that the delayed convergence to target limits the window for refinancing maneuvers. The cost of miscalibrating this timeline is exposure to sustained yield curve steepening.

Risks of Energy Shock Transmission Across Eurozone Sectors

Forward-looking price indicators confirm the energy shock is gradually feeding into other sectors of the economy. The transmission of this shock operates through the risk-taking channel, where rate changes alter enterprise asset values and risk perceptions. This mechanism creates a tangible lag, with peak effects on real GDP and inflation typically observed within 12 to 18 months of an interest rate rise. Consequently, the full impact of the June adjustment remains embedded in future quarters rather than current ledgers. Geopolitical tensions in the Middle East and energy prices serve as primary inflation drivers, distinguishing the current cycle from domestic labor-led spikes. The European Central Bank utilized artificial intelligence to change its Corporate Telephone Survey, analyzing data from approximately 70 quarterly video interviews to detect these early signals. This enhanced data collection reveals that while pass-through is occurring, it lacks the intensity seen in 2022. Operators must anticipate prolonged restrictive conditions as these sectoral impacts mature. The disconnect between immediate rate hikes and delayed economic cooling forces a defensive posture on liquidity management. Planning for a higher-for-longer plateau is not optional but a mathematical necessity the the transmission timeline.

Mechanics of Eurozone Inflation Drivers and Wage Dynamics

Defining the Price-Wage Spiral Mechanism in Eurozone Labor Markets

Rising consumer costs do not automatically trigger immediate wage demands across the Eurozone, a flexible BNP Paribas is260611~372040d313. En. Html) assesses as unlikely in the current cycle. Companies raising prices to cover labor costs while workers simultaneously demand higher pay creates an accelerating cycle, yet this reciprocal intensity remains absent because energy shocks drive the primary inflation signal rather than domestic labor markets.

| Feature | Classic Spiral | Current Eurozone Cycle |

|---|---|---|

| Primary Driver | Domestic labor tightness | Geopolitical energy costs |

| Wage Response | Immediate, aggressive indexing | Contained, lagging adjustment |

| Inflation Persistence | Self-sustaining loop | Transitory pass-through |

Transmission lags define the analytical distinction here since monetary policy impacts GDP over 12 to 18 months, a delay that prevents rapid wage-price escalation. Monetary transmission dynamics differ notably from historical precedents where labor use was absolute. Compensation growth is projected to stabilize, breaking the feedback loop before it solidifies. Operators must note that while headline numbers remain elevated, the underlying wage flexible lacks the momentum for a sustained spiral. Containment allows central banks to focus on supply-side constraints without triggering a severe demand collapse. Rate hikes will curb inflation without necessitating a deep recession to break labor pricing power.

Labor Market Durability and AI-Driven Wage Monitoring Risks

Joblessness holding near 6.3% in April 2026 sustains consumer demand while complicating the disinflationary path required by monetary policy. This historic low jobless rate prevents a deeper recession but maintains upward pressure on service sector pricing through tight labor supply. The European Central Bank mitigates this risk by deploying AI-driven analysis of corporate surveys to detect early wage settlement trends before they appear in aggregate data. Such monitoring distinguishes between one-off adjustments and the persistent feedback loops characteristic of a spiral. Despite geopolitical tensions driving energy costs, the durability of the labor market remains a primary variable in the policy calculus.

| Factor | Impact on Inflation | Monitoring Method |

|---|---|---|

| Job Availability | Sustains spending power | Survey data |

| Wage Settlements | Drives service costs | AI pattern recognition |

| Energy Costs | Raises production base | Price indices |

False positives in corporate survey interpretation could trigger premature tightening that unnecessarily suppresses growth, representing a specific operational constraint introduced by algorithmic detection reliance. Economists project another potential rate hike by the ECB in September 2026 contingent on whether these monitored wage pressures accelerate beyond current projections. A miscalculation in distinguishing temporary spikes from structural shifts would force a reversal of the higher-for-longer stance. The tension lies in maintaining restrictive policy long enough to anchor expectations without breaking the labor market dynamics that prevent a hard landing.

Strategic Application of ECB Signals for Investment Decisions

Defining the Higher-for-Longer Plateau Scenario Through 2027

Rates staying elevated instead of falling quickly defines the higher-for-longer plateau, extending pressure on rate-sensitive sectors through 2027. Historical cycles often saw the Federal Reserve initiate aggressive cutting cycles while European authorities maintained a wait-and-see approach. Transmission mechanics drive this divergence. Peak effects on real GDP typically manifest within 12 to 18 months of an interest rate rise, forcing a prolonged restrictive posture.

Premature easing creates operational risk by reigniting energy-driven price increases before initial hikes fully constrain demand. Capital allocation models must discount cash flows using sustained high discount rates rather than expecting near-term relief. The deposit facility rate anchors this extended period of restricted liquidity.

Timing Investment Strategy Adjustments Using the 12 to 18 Month Transmission Lag

Strategy adjustments must target the 12 to 18 month window following the September rate decision because this lag defines when credit tightening peaks. Cost of credit transmission to the real economy typically has a lag , meaning current GDP data fails to reflect the full impact of recent hikes. Operators acting on immediate inflation prints risk premature portfolio contraction before the transmission mechanism fully propagates.

Public spending on infrastructure is expected to underpin growth even as monetary policy restricts capital. This friction creates uncertainty. Investors should anticipate a higher-for-longer plateau extending through 2027 rather than a rapid return to neutral rates. BNP Paribas expects rates to plateau through 2027 following the projected additional hike, validating a defensive stance on duration. Pricing in rate cuts early ignores the delayed feedback loop inherent to Eurozone monetary policy. The optimal entry point for long-duration assets arrives only after the delayed GDP contraction becomes visible in hard data.

- Monitor sovereign spreads for widening signals of growth stress.

- Delay duration extension until the transmission lag effects manifest in quarterly GDP.

- Maintain exposure to sectors benefiting from defense and infrastructure spending.

- Avoid used positions until the plateau phase stabilizes post-2027.

- Reassess inflation hedges as energy shock pass-through moderates.

Interpreting the September hike as purely bullish ignores that the ECB simultaneously downgraded real GDP expectations while raising inflation forecasts. Higher yields attract capital flows, but weak economic output prevents sustained forex strength. The Federal Reserve context sharpens this risk, as US growth remains at or above trend while Eurozone expansion stagnates. Rising nominal rates coincide with deteriorating real returns, creating a trap for operators betting on currency strength. Portfolio construction requires hedging euro exposure despite the yield pickup, as the growth differential favors the dollar through 2027.

Stagflationary signals emerge where policy tightens against a slowing backdrop. Energy shocks transmit gradually to other sectors, though the pass-through remains less severe than in 2022. Compensation per employee growth is expected to slow to 3.2% in 2026 and stabilise at that level through 2027 and 2028. This contained wage outlook suggests the tightening cycle ends after one more move rather than extending into a more aggressive sequence. Markets must digest these cross-currents without expecting immediate relief from monetary authorities.

Implementation of Data-Driven Analysis for Eurozone Policy Outlook

Defining AI-Enhanced Corporate Survey Methodology

Processing approximately 70 quarterly video interviews establishes the raw data foundation for extracting inflation signals from senior company representatives. The ECB deployed artificial intelligence to change its Corporate Telephone Survey blog20260216~6ae9dd0ef0. En. Html), automating the collection and cleaning of qualitative inputs that manual analysis cannot scale efficiently. This mechanism shifts policy formulation from reactive aggregation to proactive signal detection within specific supply chains.

- Ingest raw video transcripts from scheduled corporate dialogues.

- Apply machine learning models to isolate inflation signals in text.

- Cross-reference extracted themes against purchasing managers indices. 4.

Validate September hike probability by comparing current €STR spreads against the floor system implementation where the deposit rate anchors money market pricing. The primary tension exists between persistent energy shocks and the monetary transmission lag, which delays GDP impact by up to 18 months.

- Map €STR futures curve against theECB's revised inflation trajectory.

- Isolate energy-driven components from core services inflation data.

- Assess sovereign spread widening as a leading indicator of stress.

- Confirm wage growth expectations remain anchored below spiral thresholds. Coverage Pillars recommends operators prioritize this granular verification to avoid premature portfolio contraction.

About

Marcus Halloran, Chief Market Strategist at ForexCFD. Top, brings deep interbank experience to his analysis of the ECB key rate decision. Having formerly served as an FX strategist in London, Halloran specializes in decoding monetary policy shifts and their immediate impact on G10 currency pairs like EUR/USD. His daily work involves translating complex central bank communications into actionable insights for retail traders, making him uniquely qualified to dissect the ECB's recent 25 basis point hike and forward guidance. At ForexCFD. Top, an independent publication dedicated to vendor-neutral market news, Halloran applies his expertise in interest-rate differentials to explain how rising Eurozone inflation and projected rate plateaus will influence global capital flows. This article reflects his routine focus on bridging the gap between high-level macroeconomic data and practical trading strategies, ensuring readers understand the real-world implications of the European Central Bank's tightening cycle through 2027.

Conclusion

The current trajectory reveals that monetary transmission lags will compress liquidity precisely when sovereign debt rollovers peak in late 2026. While markets focus on the immediate rate adjustment, the real fracture point emerges when stagflationary pressure forces a choice between stabilizing growth or anchoring inflation expectations. Operators relying on aggregate euro area data will miss the critical divergence between energy-dependent manufacturing hubs and resilient service economies. This blind spot creates a narrow window where sovereign spread widening accelerates quicker than policy can react, demanding a shift from passive benchmarking to active scenario stress-testing.

You must decouple your fixed-income duration strategy from the headline inflation print by Q3 2026. Do not wait for the autumn 2027 target revision; the market will price in this delay months before the official announcement. Start by auditing your portfolio's exposure to peripheral sovereign debt against rising €STR futures curves this week. Specifically, model a scenario where energy shocks persist beyond 12 months while GDP contracts below a negligible margin. This immediate granular verification prevents premature contraction and isolates capital from the delayed but inevitable drag of tight monetary policy on used sectors.

Frequently Asked Questions

The ECB raised the deposit facility rate to 2.25% effective June 17, 2026. This 25 basis point increase marks the first tightening cycle since 2023, directly impacting returns on excess liquidity held by banks across the eurozone.

The central bank now anticipates headline HICP inflation averaging 3.0% in 2026. This represents a significant upward revision from the prior 2.6% estimate, driven largely by energy costs linked to the Middle East conflict.

Growth projections have been compressed to just 0.8% for the current year. This downward adjustment reflects the restrictive monetary policy stance needed to combat persistent inflation while energy shocks transmit through various economic sectors.

Compensation per employee growth is projected to slow to 3.2% in 2026. This contained wage outlook stabilizes at that level through 2028, reducing the immediate risk of a destructive price-wage spiral emerging.

The marginal lending facility rate, serving as the corridor's upper bound, increased to 2.65%. This rate hike became effective on June 17, 2026, influencing overnight money market rates and commercial lending channels significantly.