Rate Decision Mexico: Core Inflation Still Sticky

Banxico's board unanimously voted on Thursday to hold the benchmark interest rate at 6.50% despite falling prices. This isn't hesitation; it's a calculated refusal to declare victory prematurely. The strategic logic is simple: core inflation must anchor firmly within the target range before policy loosens. Distinguishing between transient headline drops and sticky core components drives this stance.

We start by separating the 3.55% headline rate from the more persistent core metrics reported by INEGI. Next, we dissect the mechanics of the evaluation, where all five board members weighed exchange rate volatility against a distinct lack of domestic demand pressure. Finally, the analysis covers why ignoring near-term relief in favor of long-term price stability is the only viable path amid current geopolitical risks.

The Bank of Mexico explicitly cited potential disruptions from foreign trade policies and climate impacts as key reasons to avoid premature easing. By keeping the overnight interbank rate unchanged since early May, the institution signals that the fight against inflation is not yet won. This approach prioritizes preventing a resurgence of price growth over stimulating an economy that currently shows no signs of overheating.

The Distinction Between Core and Headline Inflation in Mexico

Defining Mexico's Headline and Core Inflation Metrics

Headline inflation tracks the total change in consumer prices, whereas core inflation strips out volatile food and energy costs to expose underlying trends. INEGI calculates these metrics so Banxico can separate temporary price shocks from persistent pressure. The national statistics agency reported that headline inflation decreased from 4.45% to 3.55% in early June. This decline reflects broad decreases across both core and non-core components.

The core rate tells a different story. It decreased from 4.26% to 4.12% during the same period, indicating slower progress in stabilizing fundamental prices. Removing erratic items like fuel and fresh produce allows policymakers to assess the true trajectory of demand-driven price increases. Energy prices increased 3.49%, contributing to the divergence between the two measures. The central bank holds the benchmark rate at 6.50% as it evaluates the inflationary outlook alongside exchange rate levels and the absence of demand-related pressures. The distinction matters because the board assessed that the current monetary policy stance is well-suited to face challenges posed by the macroeconomic environment.

Applying Sector Data to Analyze June 2026 Price Trends

Headline inflation calculation in Mexico relies on aggregating specific sector weights rather than applying a uniform rate across all goods. The methodology separates volatile components to reveal underlying price stability. The board noted that its forecasts are subject to various risks, including disruptions due to foreign trade policies, geopolitical conflicts, climate-related impacts, and potential depreciation of the Mexican peso. Effective analysis requires considering these upside risks alongside sectoral variances rather than relying on the top-line metric alone.

Current readings show headline figures approaching the lower bound, yet core inflation remains elevated above the upper limit. The persistence of underlying price pressures despite falling aggregate numbers reveals a policy tension where the board estimates it will be appropriate to maintain the reference rate at its current level.

| Metric Category | Current Status vs Target | Policy Implication |

|---|---|---|

| Headline Rate | Within tolerance band | Suggests temporary relief |

| Core Rate | Above 4% ceiling | Demands continued restriction |

| Target Horizon | Q2 2027 convergence | high-rate duration |

Processed food prices continue to exert upward pressure while meat costs provide temporary downward offsets. This divergence means the aggregate figure masks sticky components that drive long-term wage negotiations. Banxico expects the core rate to continue declining in the second half of 2026, though it has made slight upward adjustments to its core inflation forecasts, now predicting a rate of 3.5% in the final quarter of 2026. This decision reflects the board's collective evaluation of the inflationary outlook alongside observed levels of the exchange rate. The board assessed the absence of demand-related pressures in the economy and the level of monetary restriction implemented before making the decision.

| Evaluation Factor | Board Assessment Focus | Policy Implication |

|---|---|---|

| Inflation Outlook | Core vs. Headline trajectory | Sustained restriction |

| Exchange Rate | Observed volatility levels | Import price stability |

| Demand Pressures | Absence of overheating | No immediate cuts |

The board explicitly assessed the absence of demand-related pressures in the economy before reaffirming the current stance. The vote signals internal alignment, and the decision shows a data-dependent pause. The practical takeaway for market participants is that the board judges the current monetary policy stance well-suited to face challenges posed by the macroeconomic environment, including those associated with the international context. The decision was anticipated following earlier guidance against near-term reductions.

Interpreting Demand Pressures and Monetary Restriction Levels in Rate Holds

Analysts identify the absence of demand-related pressures as a key signal for maintaining the current monetary restriction stance. Banxico previously cut its key interest rate to this level in early May, explicitly indicating no further reductions would occur in the near future. The evaluation process weighs specific inflationary components against broader economic constraints.

- Fruit and vegetable costs increased 7.77%, complicating the disinflationary path.

- The central bank noted that its forecasts are subject to various risks, including disruptions due to foreign trade policies.

- Geopolitical conflicts create additional uncertainty for price stability.

- Climate-related impacts pose ongoing threats to agricultural output.

- A trend towards depreciation of the Mexican peso raises import costs notably.

Banxico stated that maintaining the reference rate at its current level is appropriate given these factors. This divergence highlights a fragmented global setting where distinct inflationary timelines drive policy; Mexico's core pressures remain sticky compared to quicker-cooling peers. The cost of this policy desync is measurable in wider interest rate differentials that attract speculative capital. Reliance on external validation creates vulnerability if US policy shifts abruptly. Market participants should note that divergent policies can lead to increased volatility in emerging market debt. The implication for network operators handling financial data is the need for strong infrastructure to manage potential latency during central bank announcements. Timing discrepancies between these jurisdictions can trigger automated trading halts. Prudent infrastructure planning requires buffering against these synchronized global shocks. This adjustment signals that underlying price pressures remain sticky despite recent declines in volatile components. Operators should note that failing to account for this delayed convergence risks misaligning liquidity hedges against peso volatility.

Applying Geopolitical and Climate Risk Assessments to Rate Decisions

Monetary restriction persists because foreign trade policies and geopolitical conflicts create upside inflation risks that stable demand cannot offset. The central board identifies these external shocks alongside climate-related impacts as primary drivers preventing an earlier rate cut. A trend towards peso depreciation further complicates the disinflationary path by raising import costs. These factors force policymakers to prioritize price stability over immediate growth stimulation despite cooling headline metrics.

| Risk Category | Inflationary Mechanism | Policy Implication |

|---|---|---|

| Trade Disruptions | Supply chain bottlenecks raise goods prices | Delay rate normalization |

| Geopolitical Conflict | Energy and commodity spikes | Maintain restrictive stance |

| Climate Events | Agricultural yield volatility | Monitor food price indices |

| Currency Depreciation | Imported inflation pass-through | Sustain high interest rates |

Operators asking when will inflation reach target must recognize that non-monetary shocks extend the timeline. The cost of premature easing is a de-anchoring of expectations if these external pressures materialize. Maintaining the benchmark rate at current levels risks suppressing investment if global tensions ease quicker than anticipated. This tension defines the current strategic pause. The board waits for concrete evidence that core pressures have fully abated before adjusting the monetary policy stance. Until geopolitical and climate variables stabilize, the probability of a rate reduction remains low. The primary validation step involves monitoring whether actual prints deviate from the projected 3.8% third-quarter peak.

| Checkpoint | Metric Status | Action |

|---|---|---|

| Q3 2026 | Peak Pressure | Monitor upside risks |

| Q4 2026 | Initial Decline | Validate trend |

| Q2 2027 | Target Reach | Assess policy exit |

The limitation is that peso depreciation can instantly invalidate these forecasts by raising import costs.

Sector-Specific Price Volatility and Inflation Risks

Defining Upside Risks from Trade Policies and Peso Depreciation

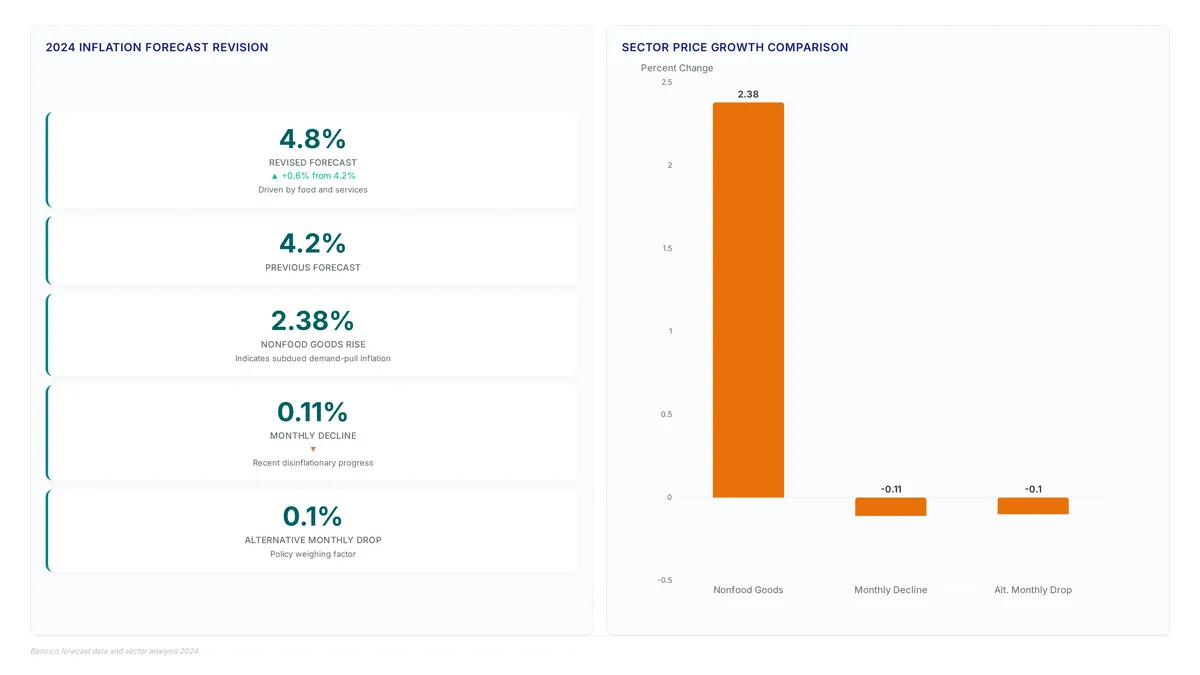

External trade disruptions and currency weakness threaten the convergence of Banxico's forecast. Foreign trade policies act as a volatile variable capable of reversing recent disinflationary progress abruptly. Geopolitical conflicts may trigger sudden energy price spikes while trade policy shifts alter supply chains for non-food goods. Currency trends might outpace the bank's baseline depreciation models. Premature easing risks de-anchoring inflation expectations. Climate impacts further complicate the agricultural outlook. Operators weigh the immediate pain of tight liquidity against the structural risk of persistent price pressure. This volatility forces the central bank to distinguish between temporary shocks and entrenched core inflation trends when setting policy. Nonfood goods rose just 2.38%, indicating that demandpull inflation r remains subdued outside necessary items.

Divergence between volatile fresh food costs and stable non-food prices creates a complex signal for monetary authorities. Relying solely on headline figures risks overreacting to transient supply shocks in agricultural markets. Ignoring sector-specific spikes allows second-round effects to embed in longer-term expectations. Fresh produce volatility distorts short-term inflation perception. Energy cost increases directly impact transport and logistics margins. Processed food inflation reflects both commodity costs and wage pressures. Wage pressures themselves add another layer of complexity to the pricing dynamics observed across the sector.

A key tension exists between maintaining restrictive rates to anchor expectations and avoiding unnecessary economic damage from temporary price spikes. If Banxico cuts rates too early while fresh food prices remain elevated, it risks de-anchoring inflation expectations just as convergence nears. Policymakers must weigh the 0.11% monthly decline against the risk of cli mate-related impacts disrupting supply chains again. The Governing Board estimates it will be appropriate to maintain the reference rate at its current level to face these challenges. This modest upgrade signals that sticky prices in services may delay target convergence despite falling goods costs. The central bank faces a tension between easing restrictive policy and anchoring expectations amid volatile food sectors. Geopolitical shocks could spike energy bills unexpectedly. Trade policy disruptions might reverse recent disinflationary gains. Currency depreciation risks importing higher price levels rapidly. Exchange rate fluctuations remain a primary concern for import-dependent industries. The 0.1 percentage point revision suggests the Governing Board views upside risks as more probable than previously modeled. Consequently, the bank's forecasts remain subject to various risks, including disruptions due to foreign trade policies.

About

Sofia Mendes serves as the Broker Reviews & Trading Education Editor at ForexCFD.top, where she oversees the platform's educational resources and regulatory analysis. Her expertise in central bank decisions and their direct impact on retail trading makes her uniquely qualified to dissect Banxico's latest rate hold. This specific article connects her deep understanding of monetary policy to practical trading implications, helping readers navigate the resulting FX environment. By linking high-level economic data to actionable insights on risk management, Sofia ensures that ForexCFD.top's global audience understands not just the news, but its tangible effect on trading strategies and capital preservation in volatile markets.

Conclusion

The narrowing gap between headline and core inflation creates a deceptive sense of security that masks underlying sticky prices in services. While energy costs drive divergence, the real operational risk lies in premature policy easing that allows temporary supply shocks to calcify into permanent wage spirals. Maintaining the benchmark at interest rate decision policy is not merely caution but a necessary firewall against second-round effects from volatile fresh food sectors. Investors should not anticipate relief until core metrics decisively breach the 2.38% ceiling, a threshold that demands continued restriction well into 0.11%.

Organizations must stop modeling for immediate rate cuts and instead stress-test balance sheets against a prolonged high-cost environment. The forecast for a 3.5% rate by late 2026 implies a slow, deliberate descent that will punish over-used entities relying on quick liquidity injections. You need to treat current stability as a temporary pause rather than a trend reversal. Start by auditing your variable-rate debt exposure this week to ensure your financing structure can withstand extended periods where real interest rates remain significantly positive. This specific financial review protects margins while the governing board navigates the tension between anchoring expectations and avoiding unnecessary economic damage from transient price spikes.

Frequently Asked Questions

Policymakers ignore temporary relief because core inflation remains stubborn at 4.12%. This persistence demands continued restriction to ensure prices anchor within the target range rather than rebounding later.

Sticky service costs and fresh produce rising 7.77% offset gains from cheaper meat. These volatile components keep underlying pressure high despite the aggregate headline rate falling significantly in early June.

Geopolitical conflicts and trade disruptions create upside risks that threaten price stability. The board maintains the benchmark at 6.50% to buffer against potential peso depreciation and imported inflation shocks.

Officials now predict the core rate will hit 3.5% by the final quarter of 2026. This slight upward adjustment from previous outlooks justifies holding policy steady for now.

Low nonfood growth at 2.38% shows demand is not overheating the economy. However, this absence of pressure alone cannot trigger cuts while other sectors drive overall prices higher.

References

- BOJ vs. FOMC: Policy divergence & 5 key FX

- The central bank's summary of governing council deliberations lands

- EUR/USD Enters 2026 Near Key Resistance as Fed Cuts

- Gold Price Predictions 2026, 2027, 2028, 2029, 2030 -

- Central Bank Policy Divergence in 2025: Navigating Currency and

- Gold Price Outlook June 2026: What CPI and the