Sovereign funds dump dollars as debt fears rise

One-third of sovereign funds plan to boost gold holdings as US debt fears mount, per Invesco data.

The era of relying on US Treasuries for portfolio stability is effectively over for global allocators. An Invesco survey of 144 institutions managing $29 trillion confirms that sovereign wealth funds are systematically dismantling traditional dollar reliance due to fears over American fiscal solvency. This is not a tactical shift but a structural rewrite of how central banks view reserve assets, driven by the collapse of the bond-equity correlation that once underpinned modern finance.

Readers will learn how 61% of central bank respondents now cite US debt as a direct threat to the dollar's reserve status, a figure that has tripled since 2024. The analysis details the operational migration away from US custodial infrastructure, where institutions are actively replacing American counterparties to mitigate sanction risks. The piece examines why gold has replaced fixed income as the primary diversifier in these fragmented markets, offering a hedge that sovereign investors can hold without counterparty exposure.

The breakdown of traditional diversification strategies forces a reevaluation of asset allocation models that dominated the previous decade. As energy security becomes a primary investment mandate, the link between physical resources and monetary reserves strengthens. This reallocation of capital represents a fundamental challenge to the post-war financial order, moving trillions in assets toward real assets and away from fiat claims that no longer guarantee stability.

The Structural Erosion of Dollar Reserve Status and Bond Correlations

US Debt Levels Eroding Dollar Reserve Currency Status

Rising US debt directly undermines reserve confidence by signaling future inflation or default risk to global holders. This structural link explains why a majority of central bank respondents stated that US debt levels negatively affect the dollar's long-term reserve currency status. Such concern has risen notably from previous years, marking a historic shift in sovereign sentiment toward greenback assets. The core problem with overreliance on dollar-denominated instruments is that fiscal deterioration erodes the very safety these assets promise. When the issuer's balance sheet expands unsustainably, the purchasing power of the currency becomes the primary adjustment mechanism.

Institutions managing $29 trillion now view this fiscal trajectory as a permanent constraint on portfolio construction. Unlike temporary market volatility, this degradation of trust alters the fundamental calculus of holding large foreign exchange reserves. The consequence is a fragmented system where safety is no longer assumed but actively engineered through non-dollar exposures. Central banks and sovereign wealth funds operate at a scale where even incremental allocation shifts move the market, compounding the impact of these sentiment changes. This shift creates an environment where higher yields are increasingly required to attract new capital. The era of assuming the dollar acts as a neutral, stable store of value regardless of US fiscal policy has ended. The driver is not short-term price action but a fundamental loss of faith in bond diversification. With traditional fixed income failing to hedge equity risk during inflation shocks, gold fills the vacuum as a neutral reserve asset.

Geopolitical fragmentation accelerates this reallocation by exposing the risks of centralized custodial infrastructure. Institutions are increasingly reviewing reliance on US-based clearing systems to avoid potential sanction use, with some European and Latin American entities already replacing US custodians or building non-US relationships. Gold offers a distinct advantage here: it carries no counterparty risk and requires no foreign legal recognition to retain value. This makes it the primary alternative for sovereign allocators seeking insulation from political friction.

The transition is characterized by a deliberate reassessment of portfolio durability rather than immediate liquidation. The sheer scale of these portfolios means even minor percentage shifts create significant market pressure. Unlike tactical traders, these entities prioritize capital preservation over yield generation. The implication for network operators and financial analysts is clear: the demand floor for gold is now institutional and structural, not speculative. While the dollar remains dominant, the margin for error in sovereign portfolio construction has vanished.

Record Deterioration in Sovereign Confidence in the Greenback

This survey records the sharpest single-year deterioration in sovereign confidence in the greenback on record in the survey's history. Such a rapid decline signals that portfolio durability now demands assets uncorrelated to US fiscal trajectories. The breakdown in traditional bond-equity diversification forces allocators to seek alternatives that preserve capital when fixed income fails as a hedge. Institutions are increasingly defining durability not by yield, but by the absence of counterparty risk within the dollar-centric custodial network. This re-evaluation suggests that even a strong dollar face value cannot offset the long-term erosion of trust among substantial holders. Consequently, sovereign allocators are redesigning portfolios to withstand a wider range of outcomes amid inflation shocks and geopolitical fragmentation. Withdrawal procedures for large-scale sovereign transfers may face increased scrutiny as entities diversify custodial relationships. Bonuses for performance based solely on yield generation will likely become irrelevant if the underlying asset class loses its reserve status. The focus shifts entirely to preserving value outside the traditional bond diversification models that dominated the previous decade.

Gold Versus Bonds as the Primary Diversifier in Fragmented Markets

Gold's Counterparty-Free Status Versus Bond Credit Risk

Gold functions as a bearer asset with no liability string, whereas bonds remain contractual claims subject to issuer solvency. This structural distinction defines diversification value when correlations break down during inflation shocks. Unlike fixed income, physical bullion requires no promise from a borrower to return principal. Sovereign investors increasingly view traditional government bonds as ineffective for equity risk protection, prompting a shift toward assets offering yield without counterparty exposure.

| Feature | Gold | Government Bonds |

|---|---|---|

| Counterparty | None | Issuer Default Risk |

| Yield Source | Price Appreciation | Coupon Payments |

| Custodial Risk | Low (Allocated) | High (Systemic) |

The limitation of this pivot is opportunity cost; UBS adjusted its year-end 2026 forecast downward to $5,500 per ounce due to persistent headwinds. Market pressure from a strong dollar and restrictive Federal Reserve policy expectations has temporarily increased the opportunity cost of holding non-yielding assets. However, the erosion of fixed income's hedge capability forces a reevaluation of portfolio durability.

Gold addresses the former while bypassing the latter entirely. This separation becomes vital as institutions redesign portfolios to withstand wider outcome ranges. The trade-off is liquidity friction versus the safety of neutral reserves.

Redesigning Portfolios for Inflation Shocks and Geopolitical Fragmentation

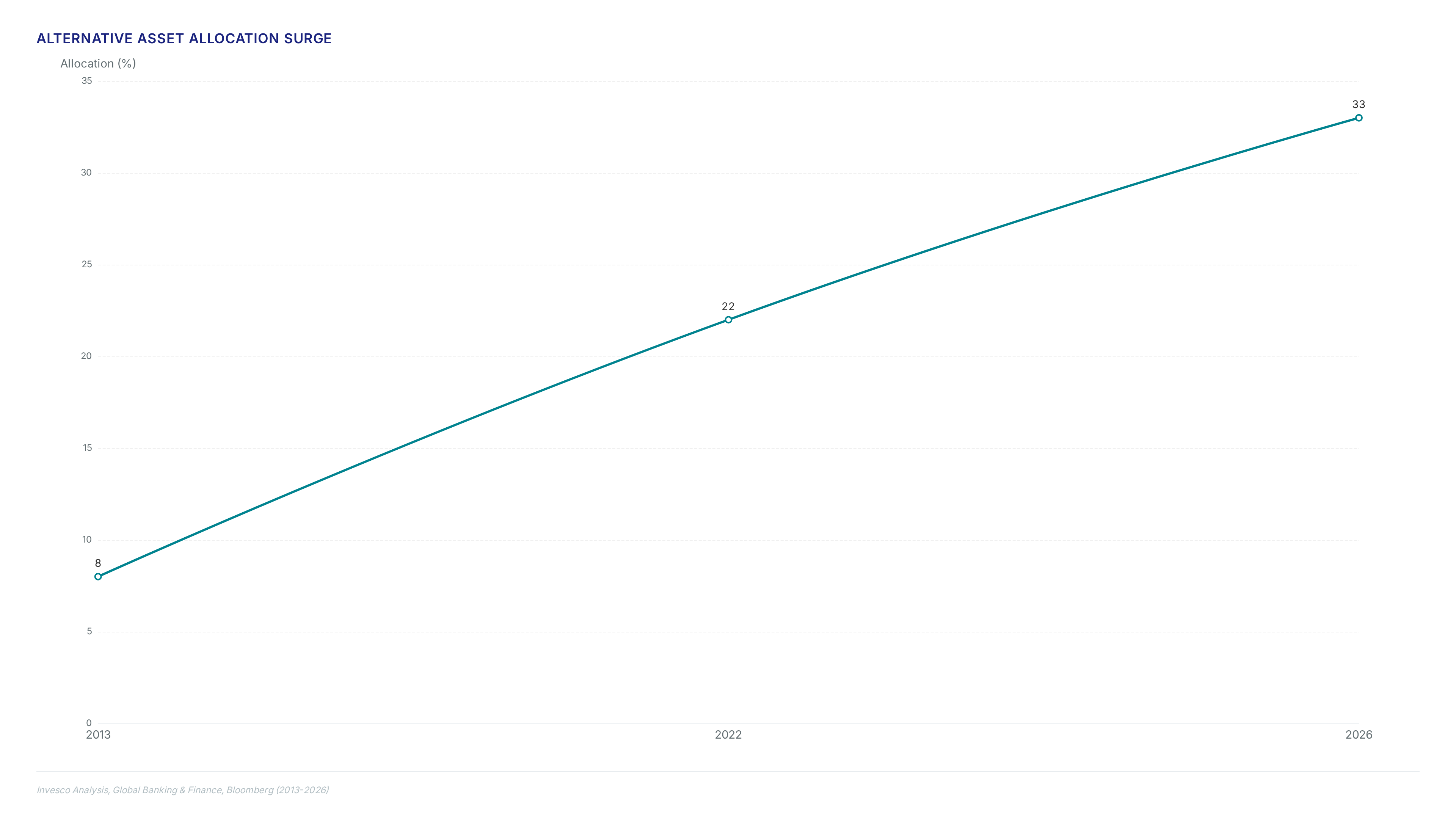

Durability has shifted from a strategic preference to a hard requirement for sovereign capital managing inflation shocks. Benjamin Jones, Invesco head of research, confirms that institutions must now withstand a wider range of adverse outcomes rather than optimizing for single-scenario returns. The primary mechanism for this redesign involves reallocating toward real assets that offer no counterparty risk. Survey data indicates that 80% of respondents identify energy security and energy transition infrastructure as the most credible investments for enhancing portfolio durability.

| Dimension | Traditional Fixed Income | Energy Transition Infrastructure |

|---|---|---|

| Correlation | Positive with equities during shocks | Low correlation to macro cycles |

| Yield Source | Coupon payments | Contractual cash flows |

| Geopolitical Risk | High (issuer dependent) | Moderate (asset backed) |

The cost of this shift is reduced immediate liquidity compared to Treasury markets. Investors trade daily mark-to-market flexibility for long-term stability against currency debasement. A critical tension exists between maintaining sufficient cash buffers for operations and locking capital into illiquid energy projects. This approach ensures capital remains deployable even when public markets seize.

Comparison: US Debt Levels Triggering Record Deterioration in Dollar Confidence

While the dollar rose roughly 3% this year on safe-haven flows, the structural pivot toward gold addresses the collapse of bond-equity diversification during inflation shocks.

| Metric | Dollar Bonds | Gold |

|---|---|---|

| Diversification | Failed (Positive Correlation) | Effective (Uncorrelated) |

| Counterparty | High (Issuer Risk) | None |

| Custodial Risk | US Infrastructure Dependent | Sanction Proof |

The Renminbi remains an unrealized alternative due to missing structural reforms, leaving gold as the primary beneficiary of this reallocation. Some bearish models suggest prices could test a lower threshold if stagflation eases, yet this ignores the non-price-sensitive nature of official sector buying. Institutions are effectively pricing in a future where fiscal dominance compromises the very collateral underpinning global trade. This shift implies that portfolio redesigns prioritize assets outside the reach of geopolitical pressure. The cost of capital in private markets now reflects this premium for non-sovereign exposure.

Operational Risks in US Custodial Infrastructure and Clearing Networks

Defining Political Exposure in US Custodial Infrastructure

Legal jurisdiction governing the clearing network creates political exposure, a factor distinct from counterparty creditworthiness. Multiple entities review reliance on US-based custodians while assessing vulnerabilities within the current framework. Hidden costs of this reliance include fragmented liquidity and settlement delays during geopolitical stress. Critics argue that non-US infrastructure lacks comparable liquidity and settlement speed. Long-term investment horizons now heavily influence sovereign comfort with political risks in emerging markets. This structural pivot ensures that capital remains accessible even during severe geopolitical fragmentation.

Case Studies: Central Banks Replacing US Custodians

Institutions evaluate methods to mitigate jurisdictional seizure risks by unwinding reliance on US financial infrastructure while building non-dollar reserve buffers. Some entities construct parallel custodial relationships outside the United States as a contingency for worst-case diplomatic deterioration. These moves signal that durability has become a hard requirement rather than a preference for sovereign capital managers. The cost of this redundancy is measurable in terms of fragmented liquidity and increased operational complexity across multiple time zones. Internal teams face a heavier burden managing disparate legal regimes. Sovereign investors view traditional government bonds as ineffective for equity risk protection, prompting a pivot toward private credit and infrastructure for yield. Unlike fixed income, physical gold offers a neutral store of value that sits entirely outside the sanction-prone clearing network. The constraint of this strategy is that any shift away from the dollar remains gradual due to the lack of a credible alternative currency with equivalent depth. Yet the directional signal is clear: official sector capital is redesigning portfolios to withstand geopolitical fragmentation even if it sacrifices some conveniences of the legacy system.

Allocated Gold Versus US-Dominated Clearing Networks

This structural separation removes the counterparty risk that forces foreign entities to rely on Washington-based intermediaries for asset safety. Gold is positioned as a natural complement to this trend because it is a neutral, sanction-proof asset that requires no custodian of the kind that generates political exposure. The vulnerability lies not in solvency but in the clearing network itself, which operates under statutes allowing asset freezes during geopolitical friction. Critics argue that exiting the dollar system sacrifices liquidity and yield, yet the opportunity cost calculation shifts when capital preservation becomes the primary mandate. Some analysts project price corrections if stagflation eases. The strategic value of holding a neutral reserve asset outweighs short-term volatility for sovereigns fearing asset immobilization. Institutional managers now treat durability as a hard requirement rather than a preference, driving capital toward assets with no political exposure. This migration creates a self-reinforcing cycle where reduced reliance on US infrastructure further isolates the dollar from global trade flows.

Implementing Non-Dollar Reserve Buffers Through Allocated Gold

Allocated Gold as a Neutral Sanction-Proof Asset

Allocated gold removes political exposure by existing outside the US-dominated clearing network entirely. Unlike dollar bonds, this physical asset requires no intermediary that Washington can legally compel to freeze holdings during diplomatic friction. The mechanism is simple: title transfers on ledgers in neutral jurisdictions, bypassing the legal seizure risks inherent in American custodial statutes. Market data shows gold trading near record highs per ounce as traders weigh restrictive policy against reserve diversification needs restrictive Federal Reserve policy.

- Verify title exists in a non-US vault to ensure sanction-proof status.

- Confirm the custodian operates under local property law, not US jurisdiction.

- Audit the chain of custody to guarantee no re-hypothecation occurs.

The limitation is liquidity depth during crisis spikes compared to Treasury markets, though UBS sees current dips as buying opportunities ahead of projected strength buying opportunities. Operators must accept that true neutrality sacrifices some yield potential for absolute sovereignty. The trade-off is operational complexity versus legal immunity from foreign statutes.

Building Non-US Custodial Relationships for Reserve Buffers

Executing a custodian migration requires mapping asset title transfers to non-US vault ledgers before terminating US clearing links. Institutions must verify that allocated gold sits outside American jurisdiction to eliminate seizure risk during diplomatic fractures. The process involves four distinct operational phases to ensure continuity of settlement while diversifying counterparty exposure.

- Audit current custody agreements to identify clauses allowing unilateral asset freezes by US authorities.

- Establish non-US custodial relationships in neutral jurisdictions such as Singapore or Switzerland for physical storage.

- Transfer title of bullion via direct ledger entry rather than through intermediate clearing banks. 4.

Validating portfolio durability requires confirming that asset structures survive inflation shocks without relying on compromised fixed income correlations. Operators must audit counterparty exposure to ensure holdings exist outside jurisdictions prone to political seizure. The failure mode often involves retaining legal title within US-dominated clearing networks while attempting to hedge against dollar debasement.

| Asset Class | Custodial Risk | Inflation Hedge |

|---|---|---|

| US Treasuries | High | Low |

| Allocated Gold | None | High |

| Infrastructure Debt | Medium | Medium |

- Verify allocated gold title rests in non-US vaults to eliminate seizure vectors.

- Confirm energy transition assets comprise a material share of the real asset bucket.

- Replace US custodians where legal statutes allow unilateral asset freezes during friction.

The cost of this validation is measurable: institutions ignoring custody jurisdiction face total loss of access despite owning the asset. While gold prices fluctuate near the $4,000 psychological level, the structural value lies in its independence from clearing houses. The limitation is that physical verification processes lag behind digital trading speeds, creating temporary liquidity gaps during crises. Durability demands accepting slower settlement for certainty of title. This approach ensures the portfolio withstands fragmentation by removing the intermediary that could block access.

About

Sofia Mendes, Broker Reviews & Trading Education Editor at ForexCFD.top, brings a unique, risk-aware perspective to the shifting dynamics of sovereign wealth funds. While her daily work focuses on vetting regulated brokers and educating retail traders on execution quality, this expertise is vital when interpreting macro-level capital flows. Mendes' rigorous methodology in analyzing regulatory frameworks and market infrastructure allows her to contextualize how institutional diversification impacts liquidity and volatility for retail participants. Her role at ForexCFD.top, an independent publication dedicated to transparent market analysis, ensures this complex topic is grounded in practical trading reality rather than speculation. By connecting high-level sovereign strategy to the tangible risks faced by traders in emerging markets, she provides the structured, evidence-based insight necessary for navigating a changing global financial environment.

Conclusion

Scaling these strategies reveals that legal title verification becomes the primary bottleneck, not market liquidity. The real cost emerges when geopolitical friction spikes, exposing those who delayed moving assets out of US-dominated clearing networks. You must prioritize jurisdictional independence over yield optimization immediately.

Commit to relocating allocated gold holdings to non-US vaults within the next six months. This timeline allows for thorough due diligence before potential regulatory windows close. Do not wait for price targets like $5,500 per ounce to validate the move; the strategic value lies in removing seizure vectors entirely. Relying on counterparty promises within compromised fixed income correlations creates a false sense of security that durability mandates cannot support.

Start this week by mapping every custodial relationship against current political risk profiles to identify single points of failure. Use available financial visualizations to track macro indicators that signal rising jurisdictional tension. This specific audit reveals where your legal title actually rests versus where you assume it sits. Only by confirming that assets exist outside statutes allowing unilateral freezes can you ensure true portfolio durability. The goal wealth preservation but guaranteed access during systemic stress.

Frequently Asked Questions

A significant 61% of central banks now cite US debt as a direct threat to reserve status. This sharp rise from 20% in 2024 forces institutions to seek non-dollar assets like gold to protect portfolio durability against fiscal erosion.

The surveyed group of sovereign wealth funds and central banks manages approximately $29 trillion in total assets. This massive scale means that even small allocation shifts away from dollar instruments create substantial structural pressure on global bond and currency markets.

Institutions are replacing US custodians to mitigate sanction risks and reduce counterparty exposure in fragmented markets. This operational shift ensures that reserve assets remain accessible and neutral, avoiding potential political friction inherent in centralized American clearing networks.

About 80% of respondents identify energy security as a primary investment mandate for building resilient portfolios. This focus drives capital toward physical infrastructure and real assets, moving away from traditional fixed income that no longer hedges equity risk effectively.

Expectations of a weaker dollar reserve role have more than doubled, rising from 12% in 2022 to 29% currently. This growing skepticism accelerates the transition toward allocated gold and other real assets that offer protection without counterparty liability.

References

- Gold Price Forecast & Predictions for 2026, 2027, 2028–2030

- Sovereign institutions and central banks | Invesco UK: Explore

- UBS targets $5,200/oz gold , sees current dip as

- Gold Price Forecast 2026: What the Major Banks Are

- Gold falls to seven-month low below $4,000 on rising

- UBS lowers 2026 gold price forecast to $5,500/oz: ‘Markets