Regulated Forex Choices: Skip Unlicensed Risks

Exactly 183 brokers hold regulated status in the 2026 landscape. That number represents the entire field of firms cleared to handle your capital under strict government oversight. Everything else is noise. This analysis cuts through the marketing fluff to examine how government-affiliated authorities actually secure your funds, dissects the mechanics of license verification, and compares hard trading conditions like use and account minimums across these vetted platforms.

The foreign exchange market operates without a single global rulebook. This fragmentation makes the line between a registered entity and an unregulated operator the only thing standing between your capital and a total write-off. Industry guides for 2026 are clear: only brokers with approval from specialized government bodies offer a transparent trading experience. Trustpilot scores have evolved from vanity metrics into primary quantitative data points, now ranked alongside spreads to measure ethical practice.

Before you deposit a dime, you must evaluate specific criteria: minimum position sizes, payment method availability, and regulatory tier. The data shows that serious regulation status is the single most necessary factor when comparing brokers, outweighing minor differences in commission structures. Firms adhering to rigorous standards allow investors to mitigate the inherent risks of a market where oversight varies drastically by region. Understanding these mechanical differences ensures your chosen forex broker provides the necessary security layer for your assets.

The Critical Role of Regulatory Oversight in Forex Trading

Defining a Regulated Forex Broker Under Tier 1 Authorities

Legal operation demands that a regulated forex broker secures authorization from a Tier 1 authority like the FCA or ASIC. Strict financial standards separate these licensed entities from unregulated operators navigating a fractured global market. Government-affiliated bodies enforce rules that create an added layer of protection for client funds. Licenses from agencies such as BaFin, CySEC, or the CFTC act as primary differentiators for trust. Transparent pricing models characterize legitimate firms, while opaque fee structures signal higher risk for traders.

Quantitative performance data now joins regulatory status in a composite evaluation methodology. Traders must verify both the license and operational metrics before depositing capital. A constraint emerges when multiple jurisdictions apply; a broker might hold a top-tier license yet onboard clients under a weaker offshore entity. The FX Brokers with Serious Regulation list curates firms meeting these rigorous criteria. Choosing a regulated intermediary guarantees a baseline of professionalism and responsibility. Regular audits provide peace of mind regarding platform integrity. Recovering lost funds after a broker failure becomes nearly impossible without this oversight. Always verify the specific license number on the regulator's official register before trading.

Applying Trustpilot Scores and Spread Metrics to Broker Selection

Validating Trustpilot scores against raw spread data confirms operational transparency when selecting a regulated broker. Modern evaluation demands more than checking a license; it requires cross-referencing user sentiment with pricing models. Industry guides now prioritize a triad of metrics comprising user scores, spread competitiveness, and commission structures Triad of metrics. This shift moves analysis from static regulatory status to flexible performance verification.

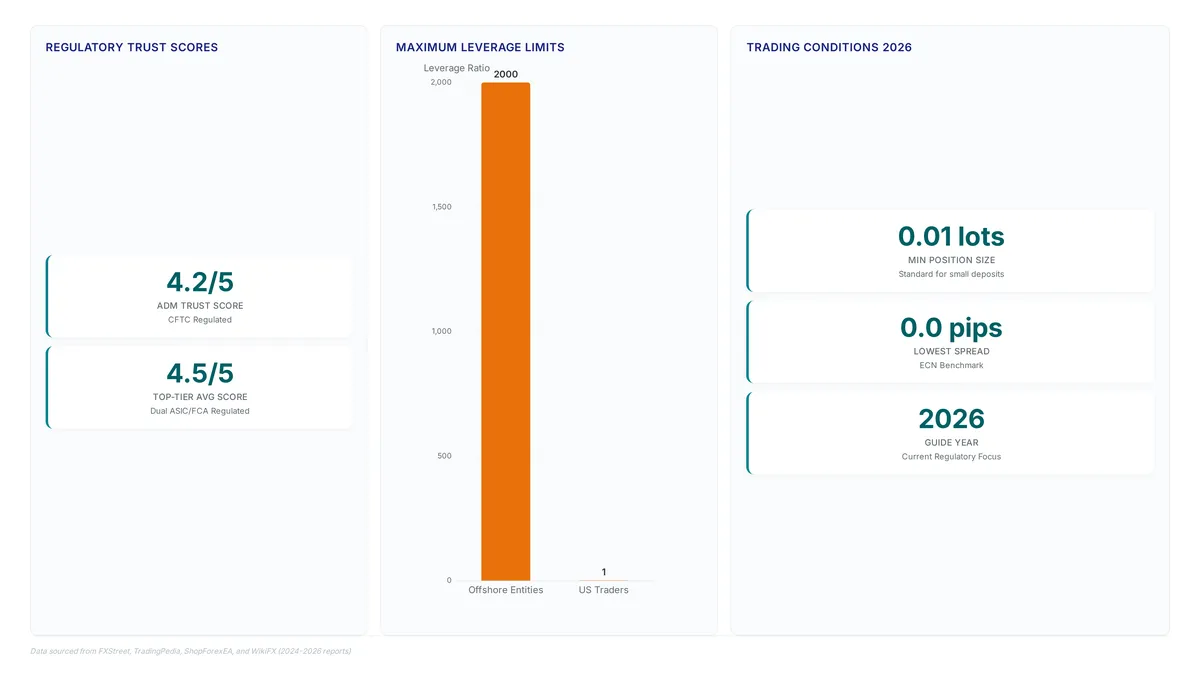

Leading regulated entities often display spreads starting from 0.0 pips, a benchmark indicating ECN architecture access rather than dealer. High user ratings on independent platforms validate these claims since false advertising triggers rapid reputation collapse. Broker ADM maintains a trust score of 4.2/5 while operating under CFTC regulation, demonstrating that strict oversight aligns with client satisfaction. Unregulated entities frequently hide costs within wide spreads, creating a hidden liability for traders.

Traders asking should I trade with a regulated broker must recognize that regulation alone does not guarantee fair pricing. A license prevents theft of principal yet poor execution can still destroy capital through excessive costs. High use offered by lax jurisdictions often masks inferior execution quality found in tightly regulated markets. Verification requires checking both the regulator's database and third-party user sentiment indexes User sentiment before deposit. This dual-layer audit protects against both fraud and systemic performance decay.

Risks of Unregulated Brokers in a Fractured Global Market

Forex regulation remains fractured without clear global rules, leaving capital exposed in unsupervised environments. Dealing through a broker that is properly registered, licensed, and supervised offers a more secure and transparent trading experience. Unregulated entities often bypass the strict financial standards required to prevent fraud and mismanagement. Total loss of deposited funds represents the primary risk since no government-affiliated body guarantees restitution.

Traders must verify that a firm holds authorization from reputable financial regulatory bodies designed to prevent fraud. A specific operational tension exists between high use offers and safety; unregulated brokers frequently advertise 1:2000 use to attract deposits they cannot cover. Supervised firms limit exposure to ensure solvency. Updated lists of compliant firms change constantly as regulatory updates and the authorization to operate are perpetual requirements for brokers wishing to remain on reputable lists in the 2026 environment. Ignoring these verification steps invites catastrophic counterparty failure. Always confirm the license status before transferring any minimum account size capital.

Inside the Mechanics of Broker Licensing and Verification

The Mechanics of Broker Licensing and Government Affiliation

Brokers must apply for a license or register with specific regional regulatory bodies to legally operate, a technical legal requirement that dictates their operational geography. This process begins when an entity submits capital proofs and compliance manuals to an authority like the FCA or ASIC. Regulators classify these bodies as Tier 1 entities, indicating a standard for regulatory seriousness. The authorization acts as a perpetual requirement, demanding continuous monitoring rather than a one-time approval. These regulations are described as providing an added layer of protection and assurance that funds are in safe hands.

| Feature | Unregulated Entity | Regulated Broker |

|---|---|---|

| Oversight | None | Continuous government agency monitoring |

| Fund Safety | Commingled accounts | Segregated client funds |

| Recourse | Formal dispute resolution | Formal dispute resolution |

The fractured nature of global forex rules means a license in one jurisdiction does not guarantee access to another. Traders often assume that a single badge implies universal acceptance, yet a broker licensed offshore may lack permission to serve clients in stricter markets. This creates a complex verification burden where the trader must cross-reference the broker's claimed status against the regulator's official register. The curated list of 183 brokers demonstrates the volume of entities claiming compliance, and dealing through a broker that is properly registered, licensed, and supervised offers a more secure and transparent trading experience. Listed brokers must adhere to strict financial standards and ethical practices to maintain their status.

Professional traders therefore treat third-party trust metrics as necessary validators rather than optional supplements. This layered approach reveals operators who maintain strict financial standards while delivering competitive trading conditions.

Checklist for Validating Tier 1 Regulatory Status and ECN Transparency

Start validation by locating the license number on the broker's website and cross-referencing it against the official FCA or ASIC registries to confirm legal entity alignment. This manual step prevents cloning scams where fraudsters mimic legitimate branding without actual authorization. Many reputable firms operate an ECN architecture to signal fair execution and transparency, contrasting with models that may involve conflicts of interest. Unlike opaque market makers, this model aggregates liquidity from multiple banks, reducing conflict of interest in trade execution. This approach marks a shift from evaluating regulation in isolation to using third-party trust metrics and transparent pricing models, such as those found in ECN structures.

| Verification Step | Action Required | Risk Indicator |

|---|---|---|

| License Check | Match ID in regulator database | ID missing or mismatched |

| Pricing Model | Confirm ECN/STP execution | Guaranteed stops advertised |

| Cost Structure | Review commission per lot | Zero commission claims |

Finally, assess third-party trust metrics alongside regulatory status, as compliance alone no longer guarantees operational excellence. High-quality firms often display competitive spreads and transparent commission structures typical of the ECN model. Traders should prioritize brokers audited by Tier 1 bodies like BaFin to ensure strict capital adequacy standards are met continuously. This approach helps identify entities that possess a license and adhere to the ethical practices required for a secure trading environment.

Comparing Key Trading Conditions Across Regulated Entities

Defining Broker Comparison Criteria: Use, Deposit, and Regulation

Effective comparison starts by quantifying Max. Use limits against specific capital thresholds. Retail traders often misinterpret high ratios like 1:2000 as inherent value rather than risk multipliers that demand strict margin discipline. While some entities offer Min. Position Size entries at 0.01 lots, the actual barrier to entry remains the Min. Account Size required to open the terminal. Regulatory status acts as the primary filter for this analysis, separating compliant venues from opaque operators.

| Broker Type | Min. Deposit | Max. Use | Regulatory Tier |

|---|---|---|---|

| Standard Retail | $10 | 1:2000 | Offshore |

| Premium ECN | $100 | 1:500 | Tier-1 Mixed |

| Institutional | $10,000 | 1:30 | Strict Local |

frameworks. Entities holding dual ASIC and FCA licenses typically enforce higher capital requirements to maintain Broker Rating integrity. This structural trade-off means traders seeking maximum use often sacrifice the legal recourse available in stricter jurisdictions. Operators must verify that Payment methods align with their region before funding any account.

RoboForex vs Exness: Comparing Use Caps and Payment Method Diversity

Both platforms offer identical Max. Use ratios of 1:2000, creating a symmetric risk profile for aggressive capital deployment. This parity means traders cannot distinguish safety based on margin multipliers alone. The divergence appears in settlement infrastructure and regulatory depth. RoboForex targets emerging market liquidity through UnionPay and Boleto Bancário, facilitating local bank transfers that bypass traditional SWIFT bottlenecks. Exness prioritizes digital asset native flows, accepting Bitcoin and Tether (USDT) alongside standard fiat gateways.

| Feature | RoboForex | Exness |

| Min. However, use symmetry masks a critical regulatory tension. |

Executing a Secure Account Opening Strategy

Application: Defining Broker Comparison Criteria for Account Selection

Start by checking the Min. Account Size against your available cash before looking at spreads. Low entry barriers mean little if the broker lacks Serious Regulation. This status acts as the primary filter for security. Operators must cross-reference Max. Use limits carefully. US traders face strict caps, whereas offshore entities may offer ratios up to 1:2000. Payment flexibility dictates operational viability. Diverse Payment methods including crypto and local transfers determine funding speed. Relying on Broker Rating scores without verifying underlying licenses exposes capital to unregulated counterparty risk. The 2026 guide year emphasizes government-affiliated oversight over commercial metrics alone. Transparent pricing structures distinguish legitimate ECN brokers from fraudulent counterparts hiding fees in wide spreads. Selecting a venue requires balancing accessibility with strict regulatory adherence to mitigate fraud.

Executing Account Opening with Crypto and Fiat Payment Methods

Match deposit preferences to specific broker capabilities before submitting identity documents. Exness accepts Bitcoin, Tether (USDT), and USD Coin (USDC) alongside standard Wire transfers. This dual-rail approach enables smooth capital deployment for crypto-native traders. Such flexibility allows operators to bypass traditional banking delays while maintaining a [Min.

| Payment Type | Supported Assets | Operational Constraint |

|---|---|---|

| Cryptocurrency | Bitcoin, USDT, USDC | Wallet address accuracy is mandatory |

| Fiat Transfer | Wire, Cards, Skrill | Subject to banking hours |

| Hybrid | Neteller, Perfect Money | Requires secondary verification |

The Min. Position Size of 0.01 lots ensures that small deposits via volatile assets like Bitcoin do not force excessive risk exposure immediately upon funding. Relying solely on cryptocurrency deposits can complicate withdrawal reversals if the initial transaction lacks sufficient blockchain confirmations. Traders must verify that their chosen entity supports withdrawals in the exact same asset class used for funding to avoid forced conversion fees. Competitive conditions in 2026 favor diverse payment options, yet the settlement finality of crypto remains distinct from fiat reversibility.

Regulatory frameworks often treat crypto-funded accounts with heightened scrutiny regarding source-of-funds documentation. A Max. Use ratio of 1:2000 may be technically available. Funding via anonymous wallets can trigger manual compliance reviews that delay trading access. Operators should prioritize brokers with clear segregation between fiat and crypto ledgers to simplify audit trails. The friction lies in balancing the speed of digital asset settlement against the rigorous anti-money laundering checks required by top-tier regulators. Always confirm the specific wallet network supported. Sending USDT via the wrong chain results in permanent loss.

Pre-Opening Validation Checklist for Use and Regulation

Verify Serious Regulation status before depositing capital to prevent immediate fund loss. Traders must confirm licensure with government-affiliated authorities rather than relying on marketing claims alone. Forex brokers operating in the US cannot offer use higher than 1:50 to retail traders due to regulatory limitations. Offshore entities may present Max. Use ratios reaching 1:2000. This creates a sharp divergence in risk exposure for global participants. Cross-referencing US Traders availability ensures compliance with local jurisdictional caps. A broker like Exness illustrates the ECN model where transparent pricing coexists with strict licensing.

| Parameter | Verification Target | Consequence of Failure |

|---|---|---|

| Regulation | FCA, ASIC, CySEC licenses | Total loss of investor protection |

| Use | Jurisdictional cap match | Forced position liquidation |

| Access | US Trader eligibility | Account rejection post-deposit |

High use availability often conflicts with the security of strict oversight. Selecting a provider with dual ASIC and FCA regulation often necessitates accepting lower use limits. This constraint ensures fair execution and prevents the hidden costs associated with unregulated manipulation. Validating these three pillars secures the trading environment against structural fraud.

About

Vikram Nair, Emerging Markets & Asia FX Writer at ForexCFD.top, brings critical on-the-ground expertise to the complex environment of regulated forex brokers. Specializing in Tier-2 and Tier-3 markets like India, Nigeria, and Southeast Asia, Vikram daily navigates the fractured regulatory environments where global rules often fail to apply uniformly. His work requires deep, practical knowledge of local legal statuses, distinguishing between fully licensed entities and unregulated operators to protect retail traders. This specific experience makes him uniquely qualified to analyze broker security, as he constantly evaluates how government affiliations impact fund safety in emerging economies. At ForexCFD.top, an independent publication dedicated to vendor-neutral analysis, Vikram applies this rigorous, scam-aware perspective to broker reviews. By connecting macro policy from bodies like the RBI and CBN to practical trading access, he ensures readers understand that choosing a properly supervised broker a recommendation, but a fundamental necessity for secure participation in the global FX market.

Conclusion

Scaling capital beyond the initial $100 deposit exposes the structural fragility of offshore use models. While 1:2000 ratios tempt aggressive positioning, they collapse under real-world volatility without the buffer of top-tier oversight. The operational cost of chasing maximum use is often total account liquidation during minor market spikes. Traders must recognize that regulatory tier dictates survival probability more than entry cost. The industry shift prioritizes government-affiliated authorities over commercial promises of unlimited access. This is not about restriction but sustainability. High-frequency strategies fail when execution relies on entities outside strict jurisdictional caps.

You should migrate to a Tier 1 regulated provider within the next thirty days if your current broker lacks dual licensing from substantial financial centers. Do not wait for a withdrawal issue to test their solvency. The specific condition for this move is matching your use needs to the jurisdictional cap rather than forcing a mismatch that invites forced liquidation. Start this week by cross-referencing your current broker's license number against the official registry of their claimed regulator. Verify that the entity holding your funds matches the one advertised on their homepage. This single step confirms whether you are trading with a protected partner or an unaccountable counterparty.

Frequently Asked Questions

Some brokers allow starting with just $10 while others require an undisclosed amount This difference determines whether you can test strategies with minimal capital or need significant funds before opening your first live account position.

Offshore entities may offer leverage up to 1:2000 whereas strict local regulators cap it lower. Higher leverage increases both profit potential and risk of rapid loss, requiring careful position sizing regardless of the broker chosen.

US traders face limited options but can find brokers with serious regulation. These firms often restrict leverage significantly compared to offshore counterparts, ensuring greater capital protection despite reduced trading flexibility for American residents.

Premium ECN accounts typically require $100 minimum deposits compared to $10 for standard retail. This higher threshold grants access to tighter spreads and direct market access, improving execution quality for active traders.

Top-tier brokers support diverse methods like PayPal and bank wires while offshore ones may limit options. This affects deposit speed and withdrawal reliability, making payment flexibility a key factor when selecting your broker.

References